Let's all do the Congo: REPCON - new issue thoughts

Stuart Culverhouse

—

Chief Economist

11 Nov 2025

Posts

Republic of Congo surprised last week with a new eurobond issued via private placement

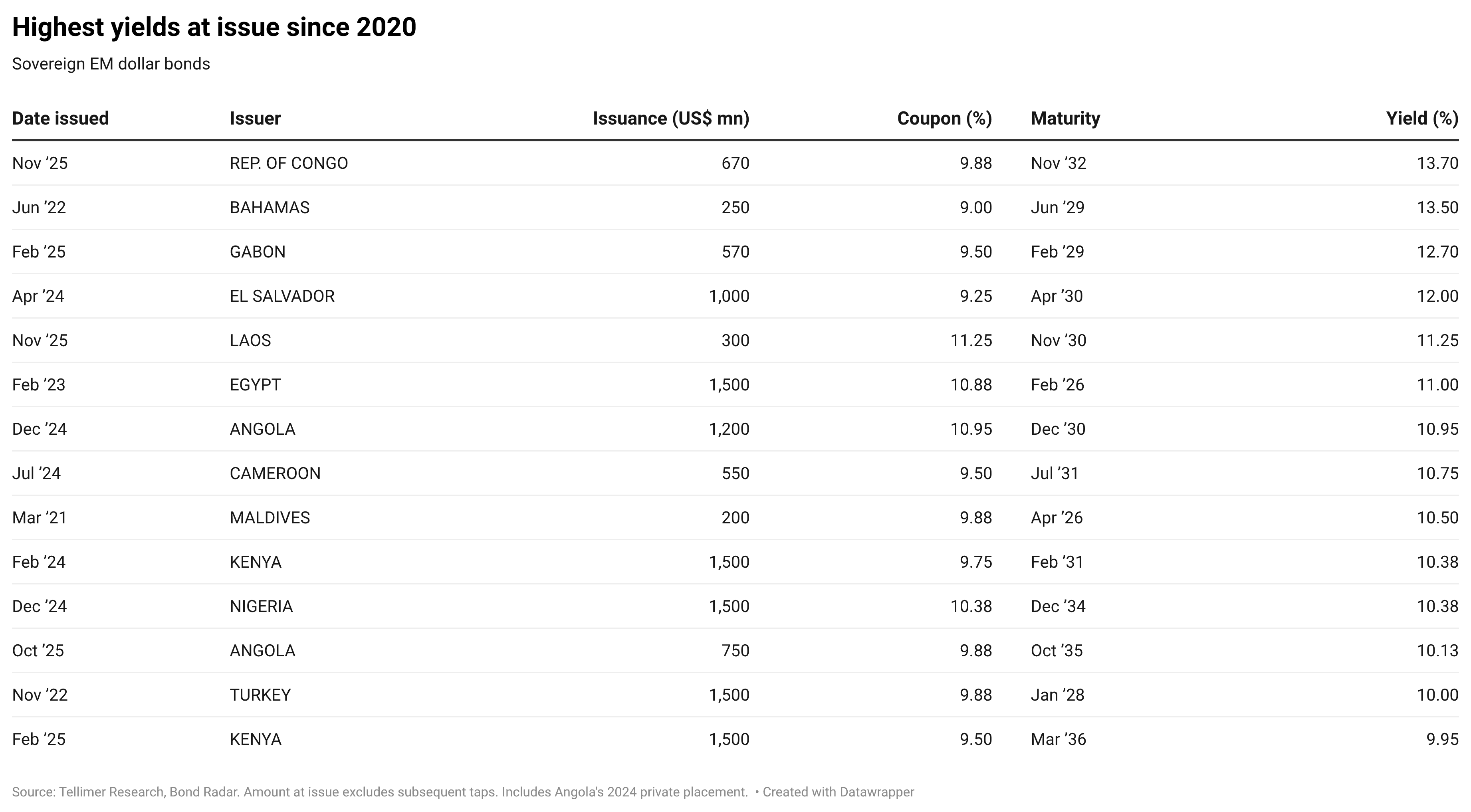

Its 13.7% yield is the highest at issue on a sovereign dollar bond in EM since 2020, if not for much longer than that

Proceeds to be used for domestic debt management purposes which may help ease local funding pressures

Republic of Congo (henceforth Congo) issued a new eurobond last week (REPCON 9.875% 2032). It is the country's second foreign bond, but its first proper issuance on the international market as its existing (and only other) bond (REPCON 6% 2029) came out of a London Club restructuring in 2007 following a HIPC debt treatment.

The new bond was priced to yield a whopping 13.7%, the highest yield at issue on a sovereign dollar bond this year (and indeed for much longer than that), in a private placement (it was issued at a heavily discounted price of US$86.728). The nominal issuance was US$670mn (although actual proceeds were only US$581mn because of the heavily discounted issue price). The bonds have an average life of 5 years (amortising in equal annual instalments over the last five years of its life, from 2028-2032). The first coupon is May 2026.

According to reports, proceeds will be used to pay off short-term treasury bonds which were issued on the regional market and fall due between November 2025 and February 2026. By this way, Congo will be able to extend the average maturity of its public debt, ease short-term refinancing pressures, and support liquidity on the CEMAC regional market (ie new external funding means it won't crowd out domestic funding). There has also been talk of a debt for nature (DFN) swap, potentially using credit guarantees, although details are vague at this stage and timing is unclear.

The issue came a bit out the blue. The private placement may have enabled the issuer to move quickly with strong interest from a small group of dedicated accounts rather than through undertaking perhaps a more time consuming public offer (which would probably require a roadshow and more heavy marketing for a relatively unknown borrower). While it is not clear what impact the different approaches would have had on the terms, we understand the bonds opened about 4pts up on the first day of trading, suggesting it was a bit mis-priced. After three days of trading, prices have since eased to around US$88 (mid price basis), as per S&P prices, up 1.5pts from re-offer (yield c13.3% on our bond calculator).

Read the full report on the Tellimer App

Stuart has over 20 years’ experience as an economist in both the public and private sectors and has been covering EMs since 2000. He joined Tellimer in July 2006 and heads the team of macro and fixed-income analysts. Previously, he worked for the UK government Economic Service and as an Economic Adviser at the Export Credits Guarantee Department.